Why now?

Studies show that 93% of millennials only invest with impact (vs. 28% for baby boomers and 55% for 40-50 year-olds).

40 of family businesses globally will hand over the reins to a new generation in the next five years

93% of millennials wish to visit every continent on earth of millennials believe social impact is key to their investing decisions.

80% of next generation business leaders say their leadership style will be different from that of their forebears.

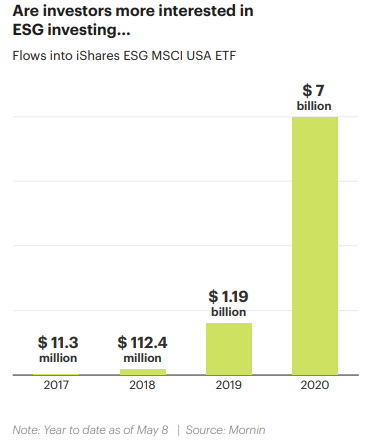

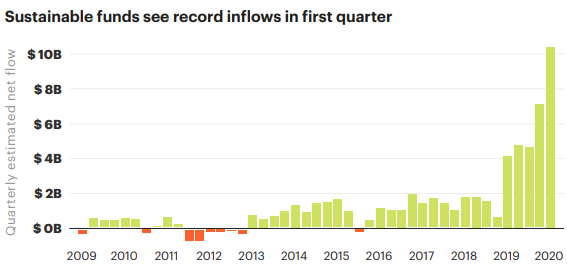

In other words, the aging and growth of the millennial and gen Z generations (which already correspond to 25% of the combined populations of Europe, US and Brazil, or 256 million) should naturally lead to increasing pressure for companies to compensate. ESG flows are booming and growing exponentially: according to Morning Star, flows have increased from US$ 112 million in 2018 to US$ 1.19 billion in 2019 and to US$ 7 billion (YTD) by July 2020.

In spite of the international media depiction of China as an environmentally unfriendly nation, recent surveys demonstrate that the Chinese climate change measures are heavily underestimated. Research shows that 73% of Chinese consider climate change to be the greatest threat to society and humanity, the highest percentage globally. It is no coincidence that China started to regulate carbon markets in its top five provinces this year.

Consumers are becoming ever more environmentally conscious, and this is leading people to compensate their carbon footprints and companies to neutralize their emissions.

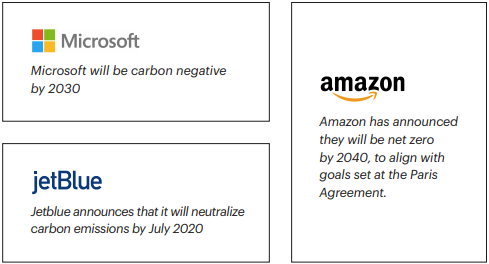

Several corporate giants, such as Amazon and Microsoft, have recently announced neutralization pledges, and this is leading to much higher compensation activity.

In addition, large companies such as Microsoft, Unilever, Verizon, Amazon, Delta, Jet Blue, among others, have already revealed in 2020 goals of offsetting the entire emissions from their production chain, generating an expectation of increasing demand for carbon credits and for credits from Amazon forest environmental projects. Amazon and Microsoft compensation alone represent 60 million tons of voluntary carbon credit demand per annum, or 12x the current supply of Brazilian Amazon forest credits.

The demand from “neutral pledges’’ announced thus far in 2020 (neutralization commitments, in which companies compensate their GHG emissions by purchases of credits in the voluntary market) has surged. There have been commitments from Apple, Amazon, Microsoft (since its founding in 1975), Bosch, Unilever, Verizon, Nike, Bradesco, Vivo, Vale (30% by 2030), BP, Shell, Repsol, Total, Starbucks, Mercedes-Benz, Google, Tesla, and many more. These neutral pledges should increase demand to more than 500 million ton / year. The airlines’ Corsia program, according to Forest Trends, will bring additional annual demand of 180 million per year from 2021 onwards.

On a global basis, the imbalance of supply and demand for voluntary carbon credits is increasing dramatically. Annual global voluntary transactions corresponded to 100 million tons in 2018 and a similar number in 2019. Hence, the current estimate is for 100 million supply growing probably to 150 million in 3 years and 100 million demand growing to 780 million in 2 to 3 years. This imbalance indicates potentially demand for carbon credits being five times larger than supply in two to three years.

It takes 2 to 3 years on average (3 to 4 years for REDD projects) for certification and addition of offer. Global supply growth is estimated at 10-20 million per year (10-20%).

As developed and wealthy countries increasingly regulate their markets, political pressure should eventually be inevitable for emerging markets to follow suit. The regulation and forced compensation of carbon emissions in developed markets lead the companies in these countries to have a competitive disadvantage (higher costs) relative to emerging market exporters, thus, we believe it might be a matter of time before lobbying by the wealthiest regulated nations at the WTO leads to the imposition of carbon tariffs against emerging markets imports. It is increasingly likely for developed market global companies to force their suppliers to compensate for their emissions. Brazil, for example, has regulated the ethanol emission allowance market (a new US$ 300 million annual market), which may be seen as a primary regulatory framework for the full compliance and regulation of the whole market.

Last updated